Debt Repayment Plan

Create a clear Debt Repayment Plan to organize what you owe and pay it off on schedule, with a free template download in PDF and DOCX.

PDF

DOC

0

likes

Download Files

- DOC

A Debt Repayment Plan is a structured document that lists everything you owe and maps out exactly how and when you will pay it back. People most often use it to take control of multiple debts, agree on terms with a creditor, or simply build a realistic schedule for becoming debt-free. You can download this Debt Repayment Plan free as a PDF or DOCX, with no signup required.

What Is a Debt Repayment Plan?

A Debt Repayment Plan is a written summary of your outstanding debts and the strategy you will follow to clear them. It can be a personal planning tool you keep for yourself, or a more formal agreement shared between a borrower and a creditor or collection agency. The document typically records each debt, the balance owed, the interest rate, the agreed monthly payment, and a target payoff date. By putting these details in one place, the plan turns a vague sense of being “behind” into a concrete, trackable path. It helps both sides understand expectations and gives you a benchmark to measure progress against each month.

When Do You Need a Debt Repayment Plan?

A repayment plan is useful any time debt feels disorganized or overwhelming. Common situations include:

- Juggling several debts at once — credit cards, a personal loan, and a store card all due on different dates.

- Negotiating with a creditor who has agreed to accept smaller, scheduled payments instead of the full balance immediately.

- Recovering from a missed payment or default, where you need a clear catch-up schedule to avoid further penalties.

- Lending money to a friend or family member and wanting a friendly but documented arrangement for repayment.

- Working toward a debt-free goal using a method like the snowball (smallest balance first) or avalanche (highest interest first) approach.

- Preparing a household budget where you need to see how much of your income is committed to debt each month.

What a Debt Repayment Plan Should Have

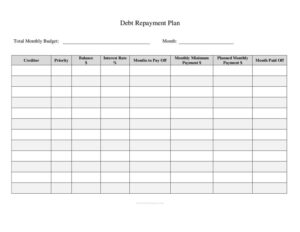

A complete plan does more than list numbers — it should be clear enough that anyone reading it understands the commitment. Strong plans include the names of the parties or creditors involved, an itemized list of each debt with its current balance and interest rate, the agreed payment amount and frequency, the start date and projected payoff date, and the method or order in which debts will be tackled. If the plan is an agreement with a creditor, it should also note any late fees, the consequences of missing a payment, and signature lines for both parties. A running balance column makes it easy to watch the total shrink over time.

How to Fill Out a Debt Repayment Plan

- Add your details. Write your name and contact information at the top, and the creditor’s name if the plan is a shared agreement.

- List each debt. Create a row for every obligation — creditor name, account number, and the current outstanding balance.

- Record the interest rate. Note the APR or interest rate for each debt so you can prioritize accurately.

- Enter minimum payments. Add the required minimum monthly payment for each account.

- Set your payment amount. Decide what you will actually pay each month per debt, including any extra you can apply.

- Choose a payoff order. Mark which debt gets the extra payment first based on your chosen strategy.

- Add dates. Fill in the start date, the day payments are due, and the projected payoff date for each debt.

- Calculate totals. Sum the balances and monthly payments so you can see the full picture.

- Sign and date. If this is an agreement with a creditor, both parties sign to confirm the terms.

Choosing a Repayment Strategy

The order in which you pay off debts can change how quickly — and how cheaply — you become debt-free. The two most popular approaches are the debt snowball and the debt avalanche. With the snowball method, you make minimum payments on everything and throw any extra money at the smallest balance first. Clearing small debts quickly builds momentum and motivation. With the avalanche method, you target the debt with the highest interest rate first, which usually saves the most money over time even if early wins feel slower. Your repayment plan supports either approach — simply mark which debt receives the extra payment and update the plan as each balance reaches zero and the freed-up money rolls into the next target.

Keeping Your Plan on Track

A plan only works if you revisit it. Update the balances at least once a month so you can see progress and stay motivated. If your income changes, a payment bounces, or a creditor adjusts your rate, revise the relevant rows rather than abandoning the document. When negotiating with a creditor, get any agreed reduction or hardship arrangement in writing and attach it to your plan. Many people also set automatic payments and calendar reminders tied to the due dates listed in their plan, which reduces the risk of late fees and keeps the schedule realistic. Treat the plan as a living document, not a one-time form.

Common Mistakes to Avoid

- Forgetting to include every debt — leaving out a small store card or a loan from family makes the totals inaccurate.

- Setting payments you can’t sustain — an overly aggressive plan that ignores living expenses often collapses within a month or two.

- Ignoring interest rates — paying down low-interest debt while high-interest balances grow can cost you significantly more.

- Not getting creditor agreements in writing — a verbal promise to accept reduced payments offers little protection.

- Failing to update the plan — a document that no longer reflects your real balances quickly becomes useless.

- Skipping an emergency cushion — putting every spare dollar toward debt with no buffer can force you back into borrowing.

Frequently Asked Questions

What is a Debt Repayment Plan used for? It is used to organize multiple debts into one clear schedule showing what you owe, how much you will pay, and when each debt will be cleared. It works as both a personal budgeting tool and a record of an arrangement made with a creditor. The goal is to replace guesswork with a concrete, trackable payoff path.

How do I fill out a Debt Repayment Plan? List each creditor with its balance, interest rate, and minimum payment, then decide how much you will pay toward each one monthly. Choose the order you’ll attack the debts, add start and target payoff dates, and total everything up. If it’s an agreement with a creditor, both parties sign and date it.

Is a Debt Repayment Plan legally binding? On its own, a personal plan you keep for yourself is not a binding contract. However, if it is signed by both you and a creditor and documents agreed terms, it can carry contractual weight. The enforceability of any such agreement varies by jurisdiction, so confirm the details with the other party.

Does a Debt Repayment Plan need to be notarized or witnessed? Most repayment plans do not require notarization or witnesses, especially when used as a personal tool. For more formal agreements involving large sums or legal disputes, some parties choose to have signatures witnessed for added assurance. Check what your creditor or local rules expect.

What’s the difference between the snowball and avalanche methods? The snowball method pays off the smallest balance first for quick motivational wins, while the avalanche method targets the highest interest rate first to minimize total interest paid. Both can be tracked with this plan. The best choice depends on whether you’re motivated more by momentum or by saving money.

How much does this Debt Repayment Plan template cost? It is completely free to download from Business Forms Pro in both PDF and DOCX formats, with no signup or payment required. You can fill it out by hand or edit the DOCX on your computer. Customize it as often as you need.

This Debt Repayment Plan template is a general example provided for informational purposes only and is not legal, financial, or tax advice. Debt and credit rules vary by jurisdiction and individual circumstances, so consult a qualified financial advisor, credit counselor, or attorney before relying on any repayment arrangement.

Official resource: for the rules that apply to your situation, see the Consumer Financial Protection Bureau.

Related Forms

- Client Income Tracker

- Open Orders Tracker

- Debt Snowball Form

- Weekly Sales Commission Tracker

- Pocket Tip Calculator

- Credit Change Notice

Browse more in Money.