Zero-Based Budget

Use this free zero-based budget template to give every dollar a job, track income and expenses, and balance to zero each month — free download.

PDF

DOCX

0

likes

Download Files

- DOCX

A zero-based budget is a planning method where you assign every dollar of income to a specific purpose until your income minus your expenses equals exactly zero. People most often use it to gain full control over their money, eliminate mystery spending, and reach goals like paying off debt or building savings. This template is free to download in PDF and DOCX with no signup required.

What Is a Zero-Based Budget?

A zero-based budget is a monthly money plan in which your total income is fully allocated across spending, saving, giving, and debt categories so that nothing is left unassigned. Unlike a traditional budget that simply tracks what you spend, a zero-based budget forces an intentional decision about every dollar before the month begins. The word “zero” does not mean you spend everything — savings and debt payments are themselves categories that receive dollars. Individuals, families, freelancers, and small business owners use this approach to make their priorities visible and to ensure income and outgo match precisely on paper each month.

When Do You Need a Zero-Based Budget?

This method works in nearly any situation where you want deliberate control over cash flow. Common scenarios include:

- You feel like money disappears each month and you cannot account for where it went.

- You are working aggressively to pay off credit cards, student loans, or other debt and want every spare dollar directed at it.

- Your income varies month to month — as with freelancers, gig workers, or commission earners — and you need to re-plan each period.

- You and a partner are trying to align on spending and want a shared, transparent plan.

- You are saving for a specific goal such as an emergency fund, a down payment, or a vacation.

- You are recovering from a financial setback and want a tight, rebuildable structure.

Types of Budget Categories to Plan

A complete zero-based budget usually groups dollars into a handful of broad buckets, and naming them clearly makes the plan easier to follow. Typical categories include income (paychecks, side income, benefits), housing (rent or mortgage, utilities, insurance), food (groceries and dining out), transportation (fuel, transit, maintenance, car payment), debt payments, savings and investing, insurance and health, and personal and lifestyle spending. Listing fixed expenses separately from variable ones helps you see which numbers you can adjust if you need to balance the plan.

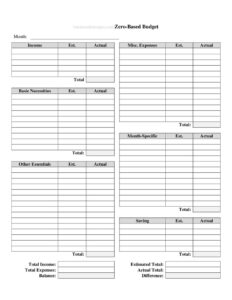

What a Zero-Based Budget Should Have

To do its job, a zero-based budget needs a few essential elements. It should clearly state the budget month or pay period it covers, a complete list of income sources with amounts, and an itemized list of expense and savings categories. It must include a running total of allocations and a final figure showing income minus expenses. The goal is for that final figure to read zero. Space for planned versus actual amounts is valuable, because it lets you compare your intentions against reality and adjust the next month.

How to Fill Out a Zero-Based Budget

- Enter the month or pay period at the top so each plan is dated and easy to file.

- List every income source — paycheck, second job, freelance work, benefits — and write the expected amount for the period. Add these to get your total income.

- Write down your fixed expenses first: rent or mortgage, utilities, insurance, loan minimums, and subscriptions.

- Add your variable expenses such as groceries, fuel, dining, and entertainment, estimating each amount.

- Assign dollars to savings and debt payoff as their own line items — treat them as bills you owe your future self.

- Total all your allocations and subtract them from total income.

- If the result is above zero, assign the leftover to a category. If it is below zero, trim a flexible category until the bottom line reads exactly zero.

- Throughout the month, record actual amounts next to your planned figures and adjust as needed.

Tips for Making Your Zero-Based Budget Stick

The plan only works if you revisit it. Build a new budget before each month or pay period rather than copying the last one blindly — your bills and goals shift. Keep a small buffer or miscellaneous category for forgotten or irregular costs so a single surprise expense does not derail the whole plan. Track spending at least weekly; catching an overrun early gives you time to move money from another category. For irregular annual costs — car registration, holidays, insurance premiums — divide the yearly amount by twelve and set that aside monthly so the bill never blindsides you. If you share finances, review the budget together so both people feel ownership.

Zero-Based Budget vs. a Traditional Budget

A traditional budget often sets category limits and lets any surplus drift into a vague “leftover” pile. A zero-based budget closes that gap by requiring every remaining dollar to be assigned, which usually directs more money toward savings and debt than people expect. The trade-off is effort: zero-based budgeting demands a fresh plan each period and more frequent check-ins. Many people find that extra structure is exactly what finally makes their goals move.

Common Mistakes to Avoid

- Forgetting irregular expenses like annual subscriptions, gifts, or car repairs, which throws the plan off when they arrive.

- Leaving income unassigned — if dollars are not given a job, they tend to vanish into casual spending.

- Being unrealistic with categories like groceries or dining, then abandoning the budget when real life exceeds the plan.

- Not tracking actual spending, so you never learn whether your estimates were accurate.

- Building the plan after the month starts rather than before, which removes its proactive power.

- Skipping a buffer category, leaving no room for the small surprises that occur every month.

Frequently Asked Questions

What does “zero-based” actually mean? It means your income minus all of your assigned dollars equals zero. Every dollar is given a specific job — including savings and debt — so none is left floating without a purpose. It does not mean your bank balance hits zero.

How do I fill out a zero-based budget? Start by listing all expected income for the month, then assign dollars to each expense, savings, and debt category. Total your allocations, subtract them from income, and adjust until the bottom line reads exactly zero. Record actual amounts as the month progresses.

Is this template legally binding? No. A zero-based budget is a personal or business planning tool, not a contract or legal document. It carries no legal obligation and simply helps you organize and direct your own money.

How often should I create a new zero-based budget? Create one for every month or pay period before it begins. Your income and bills change over time, so reusing an old plan without updating it reduces its accuracy and usefulness.

Does a zero-based budget work with irregular income? Yes, and it is one of its strengths. When income varies, base the plan on your expected or lowest reliable amount, fund your most essential categories first, then allocate any extra as the money actually arrives.

How much does this template cost? Nothing. This zero-based budget template is completely free to download in both PDF and DOCX formats, with no signup or payment required, so you can start planning immediately.

This template is a general example provided for informational purposes only and does not constitute financial, tax, or legal advice. Personal financial situations vary, and budgeting approaches that suit one person may not suit another. For guidance specific to your circumstances, consult a qualified financial professional.

Official resource: for the rules that apply to your situation, see the Consumer Financial Protection Bureau.

Related Forms

- Debt Collection Report

- Pocket Tip Calculator

- Personal Care Envelope

- Charity Cash Envelope

- Cash Flow Statement

- Tip Jar Labels

Browse more in Money.