Request For Bank Credit Reference

Download a free Request for Bank Credit Reference template to verify a client's banking history before extending credit — free PDF and DOCX download.

DOCX

0

likes

Download Files

- DOCX

A Request for Bank Credit Reference is a short business letter that asks a client’s bank to confirm details about their account history and creditworthiness before you extend credit. Companies most often use it during a credit application, when a vendor or lender needs an independent picture of how a prospective customer manages money. You can download this template free in PDF and DOCX with no signup required.

What Is a Request for Bank Credit Reference?

A Request for Bank Credit Reference is a written inquiry sent by a supplier, creditor, or finance department to a bank that a prospective customer has listed as a banking reference. It documents specific questions about the account — how long it has been open, the average balance, overdraft tendencies, and outstanding loan details — and invites the bank to confirm whether the client is satisfactory. Because bank information is confidential, the request notes that the client has authorized the disclosure. The completed reply becomes part of the credit file the requesting company keeps on hand to support its decision to approve, limit, or decline a credit line.

When Do You Need a Request for Bank Credit Reference?

This form fits any situation where you are deciding whether to trust a customer with payment terms or financing. Common scenarios include:

- A wholesaler is reviewing a new retail account that has asked for net-30 or net-60 payment terms.

- A lender or finance company is verifying the banking history listed on a credit application.

- A landlord or leasing company wants to confirm a commercial tenant’s financial stability before signing a lease.

- A B2B service provider is onboarding a large client and wants assurance before allocating resources on credit.

- A credit manager is updating the file on an existing customer who has requested a higher credit limit.

- A new supplier relationship requires references, and the client has named their bank as one of them.

What a Request for Bank Credit Reference Should Have

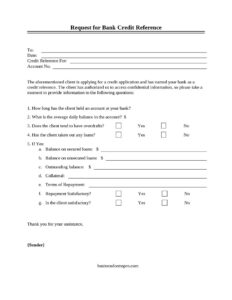

A complete request is clear, professional, and easy for a busy bank officer to answer in minutes. It should identify the bank being addressed and the date, name the client and their account number, and state plainly that the client has authorized the release of confidential information. The heart of the document is a focused set of questions about account longevity, average daily balance, overdraft behavior, loan balances, collateral, repayment terms, and overall satisfaction. Closing the letter with a courteous thank-you and the sender’s name keeps the tone professional and increases the chance of a prompt, complete reply.

How to Fill Out a Request for Bank Credit Reference

- Enter the bank’s name in the To field, addressing it to the credit reference or accounts department where possible.

- Add the Date you are sending the request.

- In Credit Reference For, write the full legal name of the client whose banking history you are verifying.

- Record the client’s Account No. so the bank can locate the correct account quickly.

- Confirm the authorization language is present, noting the client has agreed to release confidential information.

- Leave the numbered questions for the bank to complete: how long the account has been held, the average daily balance, whether the client has overdrafts, and whether they have taken out loans.

- If the client has loans, the bank fills in the secured, unsecured, and outstanding balances, plus collateral and terms of repayment.

- The bank then marks whether repayment is satisfactory and whether the client is satisfactory.

- Sign off with your name in the {Sender} field.

How to Read the Bank’s Response

Once the bank returns the completed form, the answers tell a story. A long-held account with a healthy average daily balance and no overdraft history points to stable cash management. A client who carries loans is not automatically a risk — what matters is whether repayment terms are being met and whether the bank marks repayment as satisfactory. Pay attention to the relationship between secured and unsecured balances and any listed collateral, since that indicates how leveraged the client may be. The final “Is the client satisfactory?” box is the bank’s summary judgment, but treat it as one input alongside trade references and your own credit policy rather than the sole deciding factor.

Keeping the Request Compliant and Confidential

Banks will only disclose customer information when they are confident the customer has consented. That is why the authorization language is built into this form. Keep a signed authorization or credit application from the client on file, and be ready to provide a copy if the bank asks. Store the completed reference securely, share it only with staff who need it for the credit decision, and retain it according to your company’s record-keeping policy. Disclosure rules vary, so when a bank requests its own consent form, use theirs in addition to this letter.

Common Mistakes to Avoid

- Sending the request without the client’s authorization, which leaves the bank unable to respond.

- Omitting or mistyping the account number, slowing down or blocking the bank’s reply.

- Asking for information you do not actually need for the decision, which can delay a response.

- Treating a single “satisfactory” checkbox as a complete credit assessment instead of one data point.

- Failing to address the letter to the correct department, so it sits unanswered in a general inbox.

- Not keeping a copy of the completed reference for your credit file and audit trail.

Frequently Asked Questions

What is a Request for Bank Credit Reference used for? It is used to verify a prospective or existing customer’s banking history before extending credit or payment terms. The bank confirms details such as account longevity, average balance, overdraft behavior, and loan repayment, giving you an independent view of the client’s financial reliability.

Does the client need to authorize this request? Yes. Bank account information is confidential, so the client must consent before the bank will release it. This template includes authorization language, and you should also keep a signed credit application or consent form on file in case the bank requires its own documentation.

Who fills out the form? You complete the heading details — the bank’s name, the date, the client’s name, and the account number — and sign as the sender. The bank then answers the numbered questions about the account and returns the form to you.

Is a bank credit reference legally binding? No. It is an informational inquiry and reply, not a contract. The bank’s answers help you make a credit decision, but the document itself does not obligate either party; your actual credit terms are set in your separate agreement with the client.

How long does a bank take to respond? Response times vary by institution, ranging from a few days to a couple of weeks. Addressing the request to the correct department, including the exact account number, and confirming authorization all help speed up the reply.

Is this template really free? Yes. You can download the Request for Bank Credit Reference free in both PDF and DOCX formats with no signup required, then customize it with your company details and the client’s information.

This template is a general example provided for informational purposes only and is not legal, financial, or tax advice. Confidentiality and credit-reporting requirements vary by jurisdiction and institution — consult a qualified professional before relying on it for any credit decision.

Related Forms

- Repair Under Warranty Request

- Service Call Book

- Transcript Request

- Request For Death Certificate

- Maintenance Request

- Specialty Item Form

Browse more in Request and Authorization.