Payment Calculator per $100

Use the free Payment Calculator per $100 template to estimate loan and installment payments per hundred dollars borrowed—free download in PDF and DOCX.

PDF

0

likes

Download Files

A Payment Calculator per $100 is a simple financing worksheet that shows how much you pay each period for every $100 you borrow or finance. People most often use it to compare loan offers, retail installment plans, and dealer financing on equal footing—and you can download it free in PDF and DOCX with no signup required.

What Is a Payment Calculator per $100?

A Payment Calculator per $100 is a worksheet or reference table that breaks a loan down to its smallest meaningful unit: the payment owed for each $100 of principal. Lenders, dealerships, and retailers often quote financing this way—”$4.50 per $100 per month,” for example—because it lets a buyer instantly scale the cost to any amount they want to borrow. The form documents the loan amount, the interest rate, the term, and the resulting per-$100 figure, then multiplies it back out to a full periodic payment. It is used by borrowers comparing offers, salespeople presenting financing, and finance clerks double-checking quoted numbers before a contract is signed.

When Do You Need a Payment Calculator per $100?

This worksheet earns its keep any time financing is expressed as a rate per hundred dollars or when you want an apples-to-apples comparison across offers. Common situations include:

- Comparing loan offers from two banks where one quotes a monthly dollar amount and the other quotes per $100—reducing both to the same unit reveals which is cheaper.

- Auto or equipment dealer financing, where the per-$100 figure is a familiar shorthand for estimating a monthly payment quickly on the showroom floor.

- Retail installment plans for furniture, appliances, or electronics that advertise a small per-hundred payment to make the total feel affordable.

- Personal or small-business loans where you want to know the cost of borrowing an extra $1,000 or $5,000 before deciding how much to take.

- Budgeting a purchase by working backwards: deciding how much monthly payment you can afford, then finding how much principal that supports.

- Teaching or training staff and students how interest scales with principal in a clear, intuitive way.

What a Payment Calculator per $100 Should Have

A useful version of this form captures everything needed to derive and verify the per-$100 number. At minimum it should record the loan or financed amount, the annual interest rate (APR), the term or number of payments, and the payment frequency. It should clearly show the calculated per-$100 payment, the full periodic payment, the total of all payments, and the total interest or finance charge. Including a date and a label for the lender or offer being analyzed makes the worksheet easy to file and compare later. The clearer the breakdown, the harder it is for a hidden cost to slip past you.

How to Fill Out a Payment Calculator per $100

Because this is a flexible worksheet, fill it in step by step using the figures from your quote or loan estimate:

- Date and offer label: Note today’s date and a short name for the offer (for example, “Bank A – auto loan”) so you can compare multiple sheets.

- Loan amount (principal): Enter the total amount being financed.

- Annual interest rate / APR: Record the quoted rate as a percentage.

- Term: Enter the length of the loan and the number of payments (for example, 48 months).

- Payment frequency: Indicate whether payments are monthly, biweekly, or weekly.

- Periodic payment: Calculate or copy the full payment due each period.

- Per-$100 payment: Divide the periodic payment by the principal, then multiply by 100 to get the cost per hundred dollars borrowed.

- Totals: Multiply the periodic payment by the number of payments to find the total repaid, then subtract the principal to find total interest.

With these fields filled in, you can scale the per-$100 figure to any new amount by multiplying it by the number of hundreds you plan to borrow.

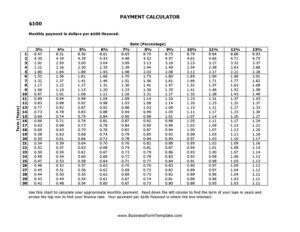

How the Per-$100 Figure Works

The math is intentionally simple. If a $10,000 loan carries a $200 monthly payment, dividing $200 by $10,000 and multiplying by 100 gives $2.00 per $100 per month. To estimate the payment on a $7,500 loan at the same rate and term, multiply 75 (the number of hundreds) by $2.00 to get roughly $150 per month. This linear scaling assumes the rate, term, and frequency stay the same; change any of those and the per-$100 figure changes too. It is an estimate, not a contract figure, but it is excellent for fast comparisons.

Tips for Comparing Offers Fairly

Always compare per-$100 figures only when the term and payment frequency match—a low per-$100 payment stretched over 72 months can cost far more in total interest than a higher one over 36 months. Look at the total interest line, not just the periodic payment, before deciding. Watch for fees, origination charges, or insurance bundled into the loan, since those can raise your true cost without changing the headline per-$100 number. When in doubt, recalculate using the APR rather than a promotional rate.

Common Mistakes to Avoid

- Comparing different terms: A lower per-$100 payment over a longer term often means more total interest, not a better deal.

- Ignoring fees: Origination, documentation, or add-on charges can make a cheap-looking per-$100 rate expensive overall.

- Mixing payment frequencies: A weekly per-$100 figure is not comparable to a monthly one without adjusting.

- Confusing rate with payment: The per-$100 figure is a payment, not an interest rate—don’t treat them as the same thing.

- Rounding too early: Round only your final answer; rounding mid-calculation skews the totals.

- Treating it as a contract: The worksheet is an estimate; rely on the lender’s official disclosure for binding numbers.

Frequently Asked Questions

What does “payment per $100” actually mean? It is the amount you pay each period for every $100 of principal financed. It lets you scale a payment to any loan size by multiplying the figure by the number of hundreds you borrow, making different offers easy to compare.

How do I calculate the per-$100 payment? Divide your full periodic payment by the loan amount, then multiply by 100. For example, a $250 monthly payment on a $10,000 loan equals $2.50 per $100 per month. Keep the term and frequency constant when scaling.

Is this calculator legally binding? No. It is an informational worksheet for estimating and comparing payments. The legally binding numbers come from your signed loan agreement and the lender’s required disclosures, such as the APR and total finance charge.

Does the per-$100 figure include interest and fees? The payment portion reflects principal plus interest for the term you enter, but it usually does not include separate fees like origination or documentation charges. Always check the total interest line and the lender’s fee schedule for the full cost.

Can I use it for any type of loan? Yes—it works for auto loans, personal loans, retail installment plans, and small-business financing, as long as the payment is fixed and regular. It is less accurate for loans with variable rates or balloon payments.

How much does this template cost? It is completely free to download here in both PDF and DOCX formats, with no signup or account required. You can fill it out by hand, edit it digitally, and reuse it for as many offers as you like.

This template is a general example provided for informational purposes only and is not financial, lending, tax, or legal advice. Loan terms, disclosure requirements, and calculation methods vary by lender and jurisdiction, so consult the lender’s official disclosures and a qualified financial professional before making borrowing decisions.

Official resource: for the rules that apply to your situation, see the Consumer Financial Protection Bureau.

Related Forms

- Hair Cash Envelope

- Credit Freeze Request

- Pocket Tip Calculator

- Client Income Tracker

- Furniture Cash Envelope

- Utilities Tracker

Browse more in Money.