Payment Calculator per $10000

Use a free Payment Calculator per $10,000 template to estimate monthly loan payments by rate and term — free download in PDF and DOCX.

PDF

0

likes

Download Files

A Payment Calculator per $10,000 is a simple reference tool that shows the estimated monthly payment for every $10,000 borrowed at a given interest rate and term. People most often use it to quickly size up loan affordability before signing anything, and it’s free to download here in both PDF and DOCX formats with no signup required.

What Is a Payment Calculator per $10,000?

A Payment Calculator per $10,000 is a worksheet or rate table that breaks loan payments down to a clean, scalable unit: the cost of borrowing exactly $10,000. Because monthly payments scale linearly with the principal, knowing the payment per $10,000 lets you multiply that figure by the number of $10,000 increments in your loan to estimate the full payment. Lenders, mortgage brokers, auto dealers, and financial educators use it as a fast comparison aid, while borrowers use it to budget. It documents the relationship between interest rate, repayment term, and the periodic payment, turning an intimidating amortization formula into a single number you can multiply.

When Do You Need a Payment Calculator per $10,000?

This tool earns its keep any time you want a quick, apples-to-apples sense of what borrowing will cost before committing. Common situations include:

- Shopping for a mortgage and comparing how a half-point rate difference changes the monthly payment per $10,000 of loan.

- Financing a vehicle at a dealership and verifying the quoted payment matches what the rate and term should produce.

- Evaluating a personal or home-equity loan where you want to know affordability before applying.

- Teaching a budgeting or financial-literacy class and needing a clear, scalable example of how rate and term drive cost.

- Refinancing existing debt and checking whether a new rate and term actually lower your monthly outlay.

- Setting a borrowing ceiling by working backward from the payment you can afford to the principal it supports.

What a Payment Calculator per $10,000 Should Have

To be useful and accurate, the worksheet should capture the three variables that determine any fixed payment, plus space to scale the result. A complete version includes: the annual interest rate, the loan term (in years or months), the resulting monthly payment per $10,000, the total loan amount you’re considering, the number of $10,000 units in that amount, and the estimated full monthly payment. Many tables also show a grid of rates against common terms (for example 15-, 20-, and 30-year columns) so you can read the per-$10,000 figure at a glance. A notes line for fees, taxes, or insurance keeps expectations realistic.

How to Fill Out a Payment Calculator per $10,000

- Enter the annual interest rate. Use the rate the lender quoted, expressed as a percentage such as 6.5%.

- Enter the loan term. Record the length of repayment, for example 30 years or 360 months. Convert years to months if your worksheet uses monthly periods.

- Find or compute the payment per $10,000. Read it from the rate-and-term grid, or calculate it using the standard amortization formula for a $10,000 principal.

- Enter your total loan amount. Write the full principal you plan to borrow, such as $250,000.

- Divide to find the number of $10,000 units. Divide the loan amount by 10,000 — $250,000 becomes 25 units.

- Multiply to get the full payment. Multiply the per-$10,000 payment by the number of units to estimate your total monthly payment.

- Add a notes line. Record any taxes, insurance, or fees that fall outside principal and interest.

How the Math Works

The strength of this tool is linearity: principal and interest payments rise in direct proportion to the amount borrowed at a fixed rate and term. If $10,000 costs $63.21 per month at a particular rate and term, then $50,000 costs five times that, or about $316.05. This lets one small table answer questions for any loan size. Just remember the per-$10,000 figure only covers principal and interest. Property taxes, homeowners or auto insurance, private mortgage insurance, and lender fees are layered on top and do not scale the same way, so your true out-of-pocket payment will usually be higher than the calculator’s base figure.

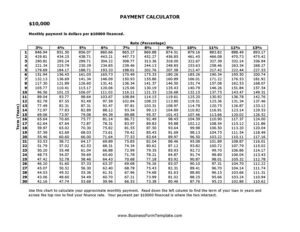

Reading a Rate-and-Term Grid

If your template includes a grid, the rows typically list interest rates in small increments and the columns list common terms. Find the row matching your rate and follow it to the column for your term — the cell where they meet is your payment per $10,000. Scanning across a row shows how a longer term lowers the monthly payment but increases total interest paid; scanning down a column shows how each rate increase raises the payment. This visual comparison is often more revealing than a single number, because it makes the cost of a higher rate or shorter term immediately obvious before you commit.

Common Mistakes to Avoid

- Forgetting taxes and insurance — the per-$10,000 figure is principal and interest only, not your full housing or auto payment.

- Mixing up term units — using a 30-year payment figure while assuming a 15-year term produces wildly wrong results.

- Using the wrong rate — the advertised rate (APR) often includes fees and may differ from the note rate used to compute payments.

- Rounding the unit count incorrectly — for a $255,000 loan you have 25.5 units, not 25.

- Assuming the rate is fixed — adjustable-rate loans change over time, so the per-$10,000 figure only holds for the fixed period.

- Treating the estimate as a quote — only your lender’s official disclosure reflects the binding numbers.

Frequently Asked Questions

What is a Payment Calculator per $10,000? It is a reference worksheet that shows the monthly principal-and-interest payment for each $10,000 borrowed at a specific rate and term. You multiply that figure by the number of $10,000 units in your loan to estimate the full payment. It turns a complex amortization formula into a single number anyone can scale.

How do I use the per-$10,000 figure for my loan? Divide your loan amount by 10,000 to get the number of units, then multiply by the per-$10,000 payment. For a $180,000 loan that is 18 units, so if each $10,000 costs $58 per month, your estimated payment is about $1,044. Always add taxes, insurance, and fees separately.

Does this include taxes and insurance? No. The per-$10,000 figure covers only principal and interest. Property taxes, homeowners or auto insurance, mortgage insurance, and lender fees are added on top, so your real monthly payment will typically be higher than the calculator shows.

Is this calculator legally binding? No. It is an estimating tool for your own planning, not a loan offer or contract. Only the lender’s official Loan Estimate or Closing Disclosure reflects the binding rate, payment, and fees you are agreeing to.

How much does this template cost? It is completely free to download here in both PDF and DOCX formats, with no signup or payment required. You can fill in the PDF by hand or edit the DOCX to add your own rates and terms.

Will the estimate change if I have an adjustable rate? Yes. The per-$10,000 payment only holds while your interest rate is fixed. With an adjustable-rate loan, the rate and therefore the payment can change after the initial period, so the calculator reflects only your current rate.

This template is provided as a general example for informational purposes only and is not financial, lending, or tax advice. Loan terms, rates, and fees vary by lender and jurisdiction. Consult a qualified financial professional or your lender before making borrowing decisions.

Official resource: for the rules that apply to your situation, see the Consumer Financial Protection Bureau.

Related Forms

- Restaurants Cash Envelope

- Accounts Receivable Form

- Savings Passbook

- Sinking Funds Tracker

- Christmas Cash Envelope

- Cash Flow Statement

Browse more in Money.