Payment Calculator per $100000

Use this free Payment Calculator per $100,000 to estimate monthly loan or mortgage payments per $100,000 borrowed — free download in PDF and DOCX.

PDF

0

likes

Download Files

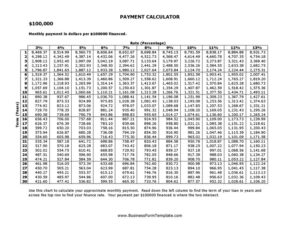

A Payment Calculator per $100,000 is a simple worksheet that shows the monthly payment required for every $100,000 of money borrowed, based on a chosen interest rate and loan term. People most often use it to quickly estimate mortgage or large-loan payments without running a full amortization schedule. It is free to download here in both PDF and DOCX formats with no signup required.

What Is a Payment Calculator per $100,000?

A Payment Calculator per $100,000 is a reference and estimating tool that expresses loan payments in a standardized unit — the cost per $100,000 financed. Lenders, real estate agents, financial planners, and borrowers use it as a quick way to compare loan options. Instead of memorizing complex formulas, you find the payment factor for a given rate and term, then multiply by the number of $100,000 increments in your loan. For example, if the payment is $500 per $100,000 and you borrow $300,000, your estimated payment is roughly $1,500. The worksheet documents the assumptions behind that estimate so anyone reviewing it understands exactly how the number was reached.

When Do You Need a Payment Calculator per $100,000?

This worksheet is useful any time you want a fast, transparent payment estimate before committing to detailed paperwork. Common situations include:

- Shopping for a mortgage — comparing how much a 30-year loan costs versus a 15-year loan at different rates.

- Setting a home-buying budget — working backward from a comfortable monthly payment to a price range you can afford.

- Refinancing decisions — checking whether a lower rate meaningfully reduces the cost per $100,000 borrowed.

- Pricing a large auto, equipment, or business loan where you want a per-$100,000 benchmark.

- Client presentations by loan officers and real estate agents who need a clean handout of payment scenarios.

- Quick rate-sensitivity checks to see how a one-point rate change affects your payment.

What a Payment Calculator per $100,000 Should Have

A complete worksheet captures every assumption that drives the result, so the estimate can be reproduced and compared. Key elements include the loan amount, the annual interest rate, the loan term in years (or months), and the resulting payment per $100,000. It should also include a field for the number of $100,000 increments and a total estimated monthly payment. Many versions add an optional column for principal and interest only versus payments that include taxes and insurance. A clearly labeled date and a notes line round out the document, recording when the rate was quoted and any assumptions that may change.

How to Fill Out a Payment Calculator per $100,000

- Enter the date and your name or client name at the top so the estimate is tied to a specific quote and time.

- Record the annual interest rate you are testing, written as a percentage such as 6.5%.

- Enter the loan term in years — for example, 15 or 30 — and convert to months if your worksheet uses months.

- Find or calculate the payment factor per $100,000 for that rate and term, and write it in the payment-per-$100,000 field.

- Enter the total loan amount you intend to borrow.

- Divide the loan amount by 100,000 to get the number of increments, and record that figure.

- Multiply the increments by the payment per $100,000 to produce your estimated monthly principal-and-interest payment.

- Add any extras such as estimated property taxes, insurance, or HOA dues if your version includes them.

- Note your final total and add any assumptions in the notes line.

How the Per-$100,000 Method Works

The strength of the per-$100,000 approach is that monthly payments scale linearly with the loan amount when the rate and term are fixed. That means the payment on $250,000 is exactly 2.5 times the payment on $100,000 at the same terms. Using a reference factor lets you build a small grid — rows for interest rates, columns for terms — and read off the payment for any loan size in seconds. This is why the method appears so often in lender rate sheets and printed mortgage tables. It keeps the math approachable while still being precise for the principal-and-interest portion of the payment.

Estimates Versus Your Final Loan Quote

Remember that this worksheet produces an estimate of principal and interest only. A real loan payment may also include property taxes, homeowners or hazard insurance, private mortgage insurance, and HOA fees, which can add hundreds of dollars per month. Lenders also charge closing costs and may quote an annual percentage rate (APR) that differs from the note rate. Treat the per-$100,000 figure as a planning baseline and always confirm the exact payment in your official loan estimate or closing disclosure before making a decision.

Common Mistakes to Avoid

- Mixing up the rate and term — using a 30-year factor with a 15-year goal will badly understate the payment.

- Forgetting taxes and insurance and assuming the principal-and-interest number is your full monthly cost.

- Using an outdated rate — rates move daily, so a factor from last month may no longer apply.

- Rounding the loan amount carelessly when calculating the number of $100,000 increments.

- Confusing note rate with APR and comparing two loans on different bases.

- Not dating the worksheet, which makes it impossible to know which rate environment the estimate reflects.

Frequently Asked Questions

What is a Payment Calculator per $100,000? It is a worksheet that shows the monthly payment for each $100,000 of money borrowed at a given interest rate and term. You multiply that factor by the number of $100,000 increments in your loan to estimate the total payment. It is a fast, transparent alternative to a full amortization calculation.

How do I use the per-$100,000 figure for my loan? Divide your total loan amount by 100,000 to get the number of increments, then multiply by the payment per $100,000. For a $400,000 loan with a $632 factor, the estimate would be 4 × $632, or $2,528 per month. Add taxes and insurance separately for a fuller picture.

Does this estimate include property taxes and insurance? No, unless your version has dedicated fields for them. The base calculation covers principal and interest only. Your actual monthly payment may be considerably higher once escrow items like taxes, homeowners insurance, and mortgage insurance are added.

Is this worksheet legally binding? No. It is an informal estimating tool, not a loan offer, contract, or commitment to lend. Only your lender’s official loan estimate and closing documents reflect binding terms, so always rely on those for final figures.

How accurate is a payment-per-$100,000 estimate? The principal-and-interest portion is mathematically accurate for the rate and term you enter, because payments scale evenly with the loan amount. Accuracy drops only if your rate, term, or loan amount changes, or if you omit taxes, insurance, or fees that apply to your real loan.

How much does this template cost? It is completely free to download from Business Forms Pro in both PDF and DOCX formats, with no signup or account required. You can print it, edit it in your word processor, or save copies for multiple loan scenarios.

This template is provided as a general example for informational purposes only and is not financial, lending, or tax advice. Interest rates, loan products, and disclosure requirements vary by lender and jurisdiction, and estimates here do not constitute a loan offer. Consult a qualified mortgage professional or financial advisor before making borrowing decisions.

Official resource: for the rules that apply to your situation, see the Consumer Financial Protection Bureau.

Related Forms

- Budget Revision Request

- Debt Payment Organizer

- Simple Payroll Cost Report

- Savings Breakdown

- Cash Receipts

- Credit Memo

Browse more in Money.