Account Statement

Free account statement template in PDF & DOCX to summarize a customer's charges, payments, and balance over a period. Bill clearly and get paid — download free.

PDF

DOCX

0

likes

Download Files

- DOCX

An account statement is a summary document that shows a customer everything that has happened on their account over a period — the starting balance, new charges, payments, and the amount now due. It’s how businesses keep customers informed and money flowing. Download this free account statement template in PDF or DOCX, fill it in, and send it. No signup required.

What Is an Account Statement?

An account statement is a periodic recap of a customer’s financial activity with your business. Rather than a single invoice for one sale, it rolls up a stretch of time — a month, a quarter, or any chosen window — into one clear picture: what the customer owed at the start, what new charges were added, what payments came in, and what’s outstanding now. Businesses that bill customers repeatedly, extend credit, or run ongoing accounts use statements to remind customers of balances, surface any disputes early, and prompt payment. For the customer, a good statement answers the only question that really matters — “how much do I owe, and for what?” — without forcing them to dig through a pile of individual invoices.

When Do You Need an Account Statement?

- Billing a customer who places multiple orders or has an ongoing account with you.

- Summarizing a month’s or quarter’s activity into a single, easy-to-read document.

- Reminding a customer of an outstanding balance to prompt payment.

- Reconciling your records against the customer’s so discrepancies surface early.

- Providing a clear running record for customers you extend credit to.

- Giving a customer the documentation they need for their own bookkeeping.

What an Account Statement Should Include

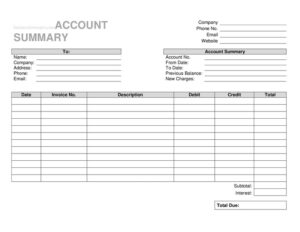

A complete statement leaves no doubt about the math. It shows your business details and the customer’s, the account number, and the period it covers (a from-date and to-date). It opens with the previous balance, lists each transaction in the period — date, invoice number, description, and the debit or credit amount — and works down to a clear closing balance. Showing each line and the running total lets the customer trace exactly how the figure was reached, which is what makes a statement trustworthy and dispute-resistant.

How to Fill Out an Account Statement

- Enter your company details — phone, email, and website — and the customer’s name, company, and contact information.

- Record the account number and the statement period (from-date and to-date).

- Enter the previous balance carried over from the last statement.

- For each transaction, list the date, invoice number, a description, and the amount as a debit (charge) or credit (payment).

- Total the new charges and the payments received, and calculate the closing balance.

- Show the amount now due and any payment terms, then send it to the customer and keep a copy.

Account Statement vs. Invoice

People often use the words interchangeably, but they do different jobs. An invoice is a bill for a single sale or batch of items — it requests payment for that specific transaction. An account statement is a summary of many transactions over a period, including invoices already sent, payments already received, and the resulting balance. Put simply, an invoice says “here’s what you owe for this order,” while a statement says “here’s everything on your account, and here’s the total still outstanding.” Many businesses send invoices as work is done and then a statement at month-end to summarize the account and nudge payment of anything still open. Used together, they keep both sides aligned and make month-end reconciliation straightforward.

Common Mistakes to Avoid

- Omitting the previous balance, so the closing figure can’t be traced.

- Listing charges without invoice numbers or descriptions, inviting disputes.

- Mixing up debits and credits, which throws off the balance.

- Forgetting to record payments received, overstating what the customer owes.

- Leaving off the statement period, making it unclear what the figures cover.

- Not keeping a copy for your own records and reconciliation.

Reconciling and Following Up on Overdue Balances

The account statement does double duty: it keeps the customer informed and it gives you a tool to get paid. Before you send one, reconcile it against your own books — confirm every invoice listed was actually issued, every payment recorded was actually received, and the closing balance ties out to your accounting records. Catching a mistake on your side before the statement goes out saves an awkward correction later and protects your credibility. Once sent, the statement becomes the natural anchor for following up on anything overdue. If a balance has aged past its terms, a brief, friendly reminder that references the statement and the specific unpaid invoices is far more effective than a vague “you owe us money” call, because the customer can see exactly what’s outstanding and why. Many businesses set a simple rhythm: send statements on the same day each month, flag any balance over thirty days, and escalate politely as an amount ages. Keeping copies of past statements also lets you show a clear history if a payment is ever disputed — you can point to the month the charge first appeared and every statement it carried on since. Used consistently, the statement turns collections from an uncomfortable, ad-hoc chore into a calm, documented routine that most customers respond to without friction, simply because the information in front of them is clear, accurate, and easy to act on.

Frequently Asked Questions

What is an account statement? It’s a summary of a customer’s account activity over a period — the previous balance, new charges, payments received, and the amount now due — presented in one clear document.

What’s the difference between a statement and an invoice? An invoice bills for a single sale; a statement summarizes many transactions over a period, including invoices and payments, to show the overall balance. Many businesses send both.

How often should I send account statements? Monthly is the most common cycle, but any regular period works. Consistent timing helps customers anticipate the statement and pay outstanding balances on schedule.

What does a debit and credit mean on a statement? A debit is a charge added to the account; a credit is a payment or adjustment that reduces the balance. Listing each lets the customer follow exactly how the closing figure was reached.

How do I fill one out? Add your and the customer’s details, the account number and period, the previous balance, each transaction as a debit or credit, and the closing balance due. The template above provides a line for each.

How much does this template cost? Nothing — it’s free to download in PDF and DOCX, with no signup required.

Official resource: for the rules that apply to your situation, see the Consumer Financial Protection Bureau.

Related Forms

- Loan Deferral Request

- Petty Cash Out

- Payment Calculator per $100000

- Saving Cash Envelope

- Pocket Payment Calculator

- Payroll Budget Estimate

Browse more in Money.