Amortization Schedule

Download a free Amortization Schedule template to map every loan payment, interest, and balance — free PDF and DOCX download, no signup.

PDF

DOCX

0

likes

Download Files

- DOCX

An Amortization Schedule is a table that breaks a loan down into every individual payment, showing how much goes to principal, how much goes to interest, and what balance remains after each installment. People most often use it to understand exactly how a loan is paid off over time and to plan for extra payments that shorten the term. You can download this Amortization Schedule template free in both PDF and DOCX formats, with no signup required.

What Is an Amortization Schedule?

An Amortization Schedule is a financial document that lays out the repayment of an installment loan from the first payment to the last. It is created by borrowers, lenders, accountants, and finance teams to track how a fixed loan balance declines over a set period. Each row of the schedule represents one scheduled payment and shows the beginning balance, the portion applied to interest, the portion applied to principal, and the ending balance. Because interest is calculated on the outstanding balance, early payments are mostly interest and later payments are mostly principal. The schedule documents this shift in plain numbers, making it a reliable reference for mortgages, auto loans, business loans, and personal financing arrangements.

When Do You Need an Amortization Schedule?

An Amortization Schedule is useful any time a loan is repaid in regular installments. Common situations include:

- Buying a home or property — to see how a 15- or 30-year mortgage splits between principal and interest each month.

- Financing a vehicle or equipment — to confirm the lender’s payment figures and total interest over the loan period.

- Taking out a business or SBA loan — to forecast cash flow and budget for fixed payments.

- Lending money privately — when one party loans funds to another and both want a clear record of how the balance reduces.

- Planning extra payments — to model how adding optional extra payments shortens the term and cuts total interest.

- Comparing loan offers — to evaluate two interest rates or terms side by side before committing.

What an Amortization Schedule Should Have

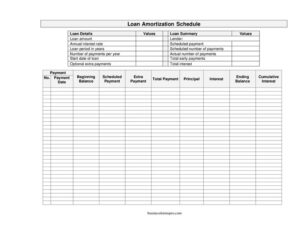

A complete Amortization Schedule combines a summary section with a row-by-row payment table. The summary captures the loan details — loan amount, annual interest rate, loan period in years, number of payments per year, and start date — along with the lender’s name. From those inputs it derives the loan summary: scheduled payment, scheduled number of payments, actual number of payments, total early payments, and total interest. The detailed table then lists every payment date with its beginning balance, scheduled payment, any extra payment, total payment, principal, interest, ending balance, and cumulative interest. Together these elements show both the big picture and the precise math behind each installment.

How to Fill Out an Amortization Schedule

- Enter the loan amount (the principal borrowed) in the loan details section.

- Add the annual interest rate as stated in your loan agreement.

- Specify the loan period in years and the number of payments per year — typically 12 for monthly payments.

- Record the start date of loan so payment dates calculate correctly.

- Enter any optional extra payments you plan to make on top of the scheduled amount.

- Fill in the lender name for reference.

- Review the auto-calculated loan summary: scheduled payment, scheduled number of payments, actual number of payments, total early payments, and total interest.

- In the payment table, confirm each payment date, beginning balance, scheduled payment, and any extra payment.

- Verify the total payment, the split between principal and interest, the ending balance, and the running cumulative interest.

How the Numbers Work

The mechanics of an Amortization Schedule rest on a simple idea: interest accrues on the remaining balance. For each period, the lender multiplies the beginning balance by the periodic interest rate — the annual rate divided by the number of payments per year — to find the interest portion. The rest of the scheduled payment reduces the principal, which lowers the next period’s beginning balance. Because the balance shrinks every payment, the interest portion falls and the principal portion rises over time, even though the total payment stays constant. The cumulative interest column adds up every interest charge paid so far, giving you a clear running total of the true cost of borrowing.

The Power of Extra Payments

The optional extra payment field is one of the most valuable parts of this schedule. Any amount paid above the scheduled payment goes entirely toward principal, which immediately reduces the balance that future interest is calculated on. Even modest extra payments can shave months or years off the loan and save a meaningful amount of total interest. The loan summary reflects this through the actual number of payments and total early payments figures, letting you see at a glance how much faster the loan is retired. Modeling different extra payment amounts before you commit helps you decide on a realistic, affordable strategy.

Common Mistakes to Avoid

- Entering the wrong payment frequency — confusing monthly with annual payments throws off every calculation.

- Using the monthly rate instead of the annual rate — always enter the annual interest rate and let the schedule divide it.

- Forgetting the start date — without it, payment dates and any prorated interest will be off.

- Ignoring extra payments already made — leaving them out makes the balance and interest totals inaccurate.

- Confusing scheduled and actual payments — extra payments reduce the actual number needed, so compare both figures.

- Not updating after a refinance or rate change — a new rate or balance requires a fresh schedule.

Frequently Asked Questions

What is an Amortization Schedule used for? It is used to map out every payment on an installment loan, showing how each payment is split between principal and interest and how the balance declines over time. Borrowers use it to budget, verify lender figures, and plan extra payments.

How do I calculate the scheduled payment? The scheduled payment is derived from the loan amount, the annual interest rate, the loan period, and the number of payments per year. This template calculates it automatically once you enter those loan details, so you do not need to do the math by hand.

Do extra payments really save money? Yes. Because extra payments go entirely toward principal, they reduce the balance that future interest is charged on, which lowers your total interest and shortens the loan term. The schedule’s actual number of payments and total interest fields show the impact.

Is an Amortization Schedule legally binding? The schedule itself is a calculation tool, not a contract. The binding terms come from your loan agreement or promissory note; the schedule simply illustrates how those terms play out over the repayment period.

Can I use this for any type of loan? Yes. It works for mortgages, auto loans, personal loans, business loans, and private lending — any loan repaid in fixed installments. Just enter the specific loan amount, rate, term, and payment frequency that apply.

How much does this template cost? Nothing. You can download the Amortization Schedule template free in PDF and DOCX formats with no signup required, and reuse it for as many loans as you need.

This template is a general example provided for informational purposes only and does not constitute financial, tax, or legal advice. Loan terms, interest calculations, and disclosure requirements vary by lender and jurisdiction — consult a qualified financial professional or your lender before making borrowing decisions.

Need to work out sales tax? Use our free Sales Tax Calculator to add or remove sales tax from any amount in seconds.

Official resource: for the rules that apply to your situation, see the U.S. Small Business Administration.

Related Forms

- Rejected Goods Notification

- Vendor Performance Warning Letter

- Sales Projection

- Cancel Back Order letter

- New Customer Form

- Election To Cancel Contract

Browse more in Sales.