General Journal

Free general journal template in PDF & DOCX. Learn what a general journal is, how double-entry journal entries work, and how to record them today.

PDF

DOC

0

likes

Download Files

- DOC

A general journal is the book of original entry where a business records its transactions in date order, using debits and credits. This printable template lays out every column you need to keep clean records. Download it free in PDF or DOCX. No signup or email required.

What Is a General Journal?

A general journal is the first place a business writes down its financial transactions, in the order they happen. Each entry records the date, the accounts affected, and the amounts as debits and credits, along with a short explanation. Because it captures transactions chronologically before they’re sorted into individual accounts, the general journal is often called the “book of original entry.” It’s the foundation of double-entry bookkeeping: every transaction is recorded here first, then posted to the relevant accounts in the general ledger. For small businesses and accounting students alike, a clear journal is what keeps the rest of the books accurate.

General Journal vs. General Ledger

These two work together but aren’t the same. The general journal records transactions *chronologically* — a running diary of what happened and when. The general ledger organizes those same transactions *by account* — all the entries for “Cash,” all the entries for “Sales,” and so on — so you can see the balance of each account. The flow is simple: you record a transaction in the journal first, then “post” it to the matching accounts in the ledger. The journal tells the story in time order; the ledger sorts that story by account.

The Basics of Double-Entry

Every journal entry follows one unbreakable rule: total debits must equal total credits. That’s the heart of double-entry bookkeeping. Each transaction affects at least two accounts — for example, buying supplies for cash increases the Supplies account (a debit) and decreases the Cash account (a credit) by the same amount. This built-in balance is what makes errors easy to spot: if the debits and credits in an entry don’t match, something is wrong. The template’s “total debits” and “total credits” lines are there to help you confirm the entry balances before you move on.

When Do You Use a General Journal?

- Recording day-to-day business transactions in date order

- Entering adjustments, corrections, or end-of-period accruals

- Logging transactions that don’t fit a specialized journal (sales, purchases, cash)

- Teaching or learning the fundamentals of double-entry bookkeeping

- Keeping a clear audit trail before posting to the ledger

What a Journal Entry Includes

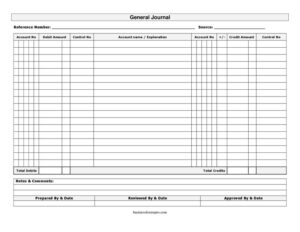

A complete entry leaves no ambiguity about what happened. The template captures the date, a reference number, and the source of the transaction, then for each line the account number, account name/explanation, and the debit or credit amount, with a control number where needed. It totals the debits and credits so you can confirm they match, and finishes with notes and signature lines for who prepared, reviewed, and approved the entry — useful for businesses that separate these duties for control.

How to Fill Out a General Journal

- Enter the date of the transaction and a reference number to identify it.

- Note the source (an invoice, receipt, or document the entry is based on).

- For each account affected, write the account number and account name/explanation.

- Record the amount in the debit or credit column — debits on the accounts that increase in value or assets, credits on the others.

- Add the debit and credit totals and confirm they are equal before moving on.

- Add any notes, and have the entry prepared, reviewed, and approved with dates where your process requires it.

A Simple Example

Say a business pays $200 cash for office supplies. The journal entry debits “Office Supplies” $200 (the asset increases) and credits “Cash” $200 (the asset decreases). Total debits ($200) equal total credits ($200), so the entry balances. The explanation line might read “Purchased office supplies for cash.” Posted to the ledger, this entry raises the Office Supplies account and lowers the Cash account — and anyone reviewing the books can trace exactly what happened and why.

Common Mistakes to Avoid

- Debits and credits that don’t add up to the same total

- Forgetting the explanation, so the entry’s purpose is unclear later

- Recording the amount in the wrong column (debit vs. credit)

- Skipping the reference or source, breaking the audit trail

- Letting entries pile up instead of recording them promptly

Tips for Accurate Journal Entries

A few habits keep your journal reliable. Record each transaction as soon as it happens, while the details are fresh and the source document is in hand. Write a clear explanation for every entry — months later, “transfer” tells you nothing, but “transferred $500 from checking to the payroll account” tells you everything. Double-check that debits equal credits before moving on, since catching an imbalance now is far easier than hunting for it at month-end. Keep your reference numbers sequential so nothing is lost, and file the source documents where they can be matched back to the entry. Consistent, prompt entries are what make the rest of your books trustworthy and your year-end far less stressful.

Frequently Asked Questions

What is a general journal? It’s the book of original entry where a business records transactions in date order using debits and credits, before posting them to the general ledger.

What’s the difference between a general journal and a general ledger? The journal records transactions chronologically; the ledger organizes those same transactions by account so you can see each account’s balance.

What is a general journal entry? A single record of one transaction, showing the date, the accounts affected, and the debit and credit amounts — which must be equal.

Why must debits equal credits? Because double-entry bookkeeping records every transaction in at least two accounts of equal value. If debits and credits don’t match, the entry contains an error.

When is a general journal page complete? When every transaction for the period is recorded and each entry balances, with the debit and credit totals agreeing — ready to post to the ledger.

How much does this template cost? It’s free to download in PDF and DOCX.

Related Forms

Cash Receipts · Account Reconciliation Form · Check Register · Petty Cash · Balance Sheet

This template is provided for general informational purposes only and is not financial or accounting advice. Consult a qualified accountant for your bookkeeping and reporting needs.

Related Forms

- Household Inventory Card

- Stock Requisition Form

- Weekly Music Practice Log

- College Application Comparison Checklist

- Inventory Cards

- Social Security Options Planner

Browse more in Log and Inventory.