Truth In Lending Statement

Download a free Truth In Lending Statement template that clearly discloses your loan's APR, finance charge, and payment terms — free PDF and DOCX download.

PDF

DOCX

0

likes

Download Files

- DOCX

A Truth In Lending Statement is a loan disclosure document that lays out the true cost of borrowing — the annual percentage rate, finance charge, amount financed, and payment schedule — in one standardized place. Borrowers most often receive it when applying for a mortgage, auto loan, or other installment credit so they can compare offers on equal footing. You can download this template for free in PDF and DOCX, with no signup required.

What Is a Truth In Lending Statement?

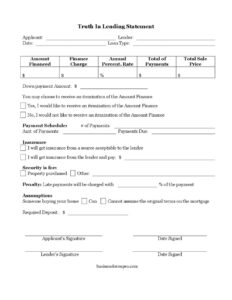

A Truth In Lending Statement is a written disclosure a lender gives a borrower that summarizes the key financial terms of a credit transaction. Rooted in consumer-protection principles, it translates a loan into a handful of clearly labeled numbers: the Annual Percentage Rate (APR), the total Finance Charge, the Amount Financed, and the Total of Payments. It also spells out the payment schedule, any required insurance, security interests, late penalties, and whether the loan can be assumed. The purpose is transparency — letting a consumer see exactly what they are agreeing to and how much credit will ultimately cost before they sign.

When Do You Need a Truth In Lending Statement?

This form appears whenever a lender extends consumer credit and needs to disclose its real terms. Common situations include:

- Mortgage and home loans — buyers receive a statement showing the APR, total interest paid over the life of the loan, and the monthly payment schedule.

- Auto financing — a dealer or lender discloses the amount financed, down payment, and the total sale price of the vehicle on credit.

- Personal installment loans — a borrower sees the finance charge and number of fixed payments before accepting funds.

- Refinancing an existing loan — the new terms, rate, and payment schedule are presented for comparison against the old loan.

- Secured loans — when collateral such as purchased property backs the loan, the statement identifies the security interest.

- Loans with required deposits or insurance — the document discloses any deposit the borrower must hold or insurance they must carry.

What a Truth In Lending Statement Should Have

A complete statement makes the cost of credit unmistakable. At a minimum it should include the names of the applicant and lender, the date, and the loan type. The four core figures — Amount Financed, Finance Charge, Annual Percentage Rate, and Total of Payments — must be displayed prominently, often in a boxed format. It should also state the Total Sale Price and Down Payment Amount where a purchase is involved, a detailed payment schedule, insurance arrangements, the security interest, any late-payment penalty, assumption rights, and any required deposit. Finally, it needs signature lines and dates for both the applicant and the lender so each party acknowledges the disclosed terms.

How to Fill Out a Truth In Lending Statement

- Enter the Applicant name, the Lender name, and the Date the disclosure is prepared.

- Specify the Loan Type (for example, mortgage, auto, or personal installment).

- Fill in the four headline figures: Amount Financed, Finance Charge, Annual Percentage Rate, and Total of Payments.

- Record the Total Sale Price and the Down Payment Amount if the loan funds a purchase.

- Let the applicant check whether they want an itemization of the Amount Financed — Yes or No.

- Complete the Payment Schedule: the number of payments, the amount of each payment, and when payments are due.

- Indicate the Insurance arrangement — obtained from an acceptable source or purchased through the lender for a stated amount.

- Identify what the Security is for (property purchased or other) and note any late-payment penalty percentage.

- Mark whether someone buying the home can or cannot assume the original terms, list any Required Deposit, then have both parties sign and date.

Understanding the APR vs. the Interest Rate

One of the most useful features of this statement is the distinction between the stated interest rate and the Annual Percentage Rate. The interest rate reflects only the cost of borrowing the principal, while the APR rolls in certain fees and charges to express the loan’s total yearly cost as a single percentage. Because the APR captures more than just interest, it is usually higher than the nominal rate. Comparing the APR across competing loan offers — rather than comparing only monthly payments or sticker rates — gives a more honest picture of which loan is genuinely cheaper over time. The Finance Charge, meanwhile, shows the dollar total you will pay for credit across the life of the loan.

The Itemization, Insurance, and Assumption Sections

The itemization option lets a borrower request a line-by-line breakdown of how the Amount Financed was calculated, which is helpful for spotting unexpected fees. The insurance section clarifies whether coverage is required and, if so, whether it must come from the lender at an added cost or from an outside provider the lender finds acceptable. The assumption clause matters mostly for mortgages: it tells a future buyer whether they could take over the existing loan on its original terms or whether the balance would have to be refinanced. Reviewing these sections closely prevents surprises later in the loan’s life.

Common Mistakes to Avoid

- Confusing the APR with the interest rate — they are different numbers, and the APR is the one to compare across offers.

- Leaving the payment schedule blank or incomplete — the number, amount, and due dates of payments must all be filled in.

- Skipping the itemization checkbox — failing to choose Yes or No can delay processing or leave the borrower without a fee breakdown.

- Overlooking the insurance terms — not noticing that coverage must be bought through the lender can add unexpected cost.

- Ignoring the late-payment penalty — the percentage charged on missed payments should be understood before signing.

- Signing without dating — both the applicant and lender signature lines need corresponding dates to document when terms were disclosed.

Frequently Asked Questions

What is a Truth In Lending Statement used for? It is used to disclose the real cost of a loan to a borrower in a clear, standardized format. By presenting the APR, finance charge, amount financed, and payment schedule together, it lets consumers understand and compare credit terms before agreeing to them.

How do I fill out a Truth In Lending Statement? Start with the applicant and lender details, then enter the loan’s core figures — amount financed, finance charge, APR, and total of payments. Complete the payment schedule, insurance and security sections, note any penalties or required deposit, and have both parties sign and date the form.

What is the difference between APR and the finance charge? The APR expresses the yearly cost of credit as a percentage, including certain fees, while the finance charge is the total dollar amount you pay for the credit over the life of the loan. Both appear on the statement and serve different comparison purposes.

Does a Truth In Lending Statement need to be notarized? Notarization is generally not required for this disclosure. It typically just needs the dated signatures of the applicant and lender to document that the terms were presented and acknowledged.

Is this statement legally binding? The statement documents the disclosed terms of a loan, and signing acknowledges receipt of those terms. The binding obligations usually arise from the underlying loan agreement; requirements and the exact role of this disclosure vary by jurisdiction and loan type.

How much does this template cost? This Truth In Lending Statement template is completely free to download here in both PDF and DOCX formats, with no signup required. You can customize the fields to match your specific loan and reuse it as needed.

This template is a general example provided for informational purposes only and is not legal, financial, or tax advice. Lending disclosure requirements vary by jurisdiction and by the type of credit involved. Consult a qualified attorney or financial professional before relying on this document for any specific transaction.

Official resource: for the rules that apply to your situation, see the Consumer Financial Protection Bureau.

Related Forms

- Why Denied Credit letter

- Request Credit Card Chargeback

- Emergency Cash Envelope

- Payment Calculator per $10000

- Accounts Receivable Form

- Income Statement

Browse more in Money.